Europe's airline capacity begins slow climb

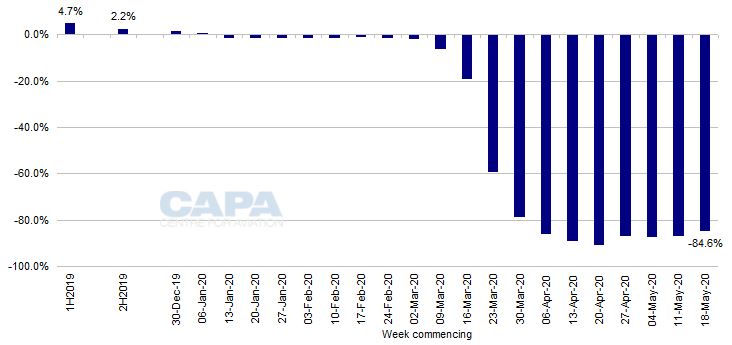

Total seat numbers in Europe are down 84.6% year-on-year in the week of 18-May-2020, according to schedules from OAG combined with CAPA Fleet Database seat configurations.

This is almost 2ppts narrower than the previous week's 86.5% drop and the smallest rate of decline since Mar-2020. Nevertheless, it is the seventh successive week of cuts broadly in the -85% to -90% range.

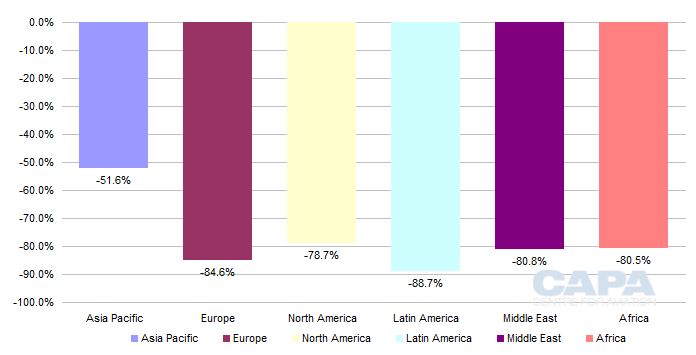

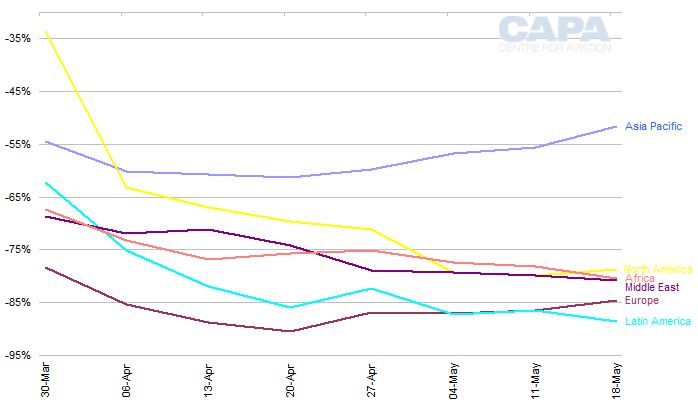

Europe's cuts are no longer the world's deepest. That distinction now belongs to Latin America, where seats have dropped by 88.7% year-on-year. Seats are down by 80.8% in Middle East, 80.5% in Africa, 78.7% in North America and 51.6% in Asia Pacific. The rate of fall is narrowing in the three big regions - Asia Pacific, Europe and North America - but widening in the others.

Data based on filed schedules indicate that European aviation may be at the beginning of a slow rebuilding of capacity.

However, plans by Ryanair, IAG, Lufthansa and Air France-KLM imply that capacity for Europe's leading groups will still be reduced by around 50%-80% in Jul-2020. Even those plans are based on the lifting of restrictions.

- Total seat numbers in Europe are down 84.6% year-on-year in the week of 18-May-2020.

- Europe no longer has the deepest cut in seat capacity, with Latin America now falling faster.

- Asia Pacific, Europe, and North America are showing signs of an upward trend in seat capacity, while other regions continue to decline.

- The U-shaped recovery in Europe's aviation industry is widening, with capacity for June 2020 projected to be down by 34% year-on-year.

- However, scheduled capacity for July 2020 has increased and is expected to be within 6% of July 2019 levels.

- The filed schedules of Europe's major airline groups are overly optimistic, with actual operations likely to be at much lower capacity levels. Further cuts to filed schedules are expected.

Summary

- Europe: 5.1 million seats vs 33.4 million a year ago - a fall of 85%. Europe no longer has the deepest cut (Latin America is now falling faster).

- The U-shaped recovery is still widening, with Jun-2020 capacity falling, but Jul-2020 scheduled capacity has increased.

- Schedules for Europe's big five airline groups are way ahead of likely reality this summer. There will be further cuts to filed schedules.

Europe: 5.1 million seats vs 33.4 million a year ago - down by 85%

Total European seat capacity is scheduled to be 5.1 million seats in the week of 18-May-2020.

This is a 1.9% increase week-on-week, but is still 84.6% below the 33.4 million seats of the equivalent week a year ago, according to the data from OAG/CAPA.

The total is split between 1.5 million domestic seats, versus 7.8 million last year; and 3.7 million international seats, versus 25.6 million.

Europe's domestic seats have dropped by 81.0% (a lesser cut than last week's -82.0%); international by 85.7% (a slightly narrower cut than last week's -87.9%).

The 84.6% year-on-year cut in total seats this week compares with -86.5% in the week of 11-May-2020, which had been the third successive week of cuts of around 87% following the low point of -90.4% in the week of 20-Apr-2020.

This is the ninth week of very heavy double digit percentage (more than 50%) declines in seats.

This week's cut is the narrowest rate of decline since seat numbers fell by 78.1% in the week of 30-Mar-2020. In absolute terms, this week's total of 5.1 million seats is also the highest since that same week, when it was 6.7 million.

However, Europe's capacity can still be characterised as bumping along the bottom.

See related report: Europe's airline capacity bumps along the bottom; lockdowns ease

Europe: year-on-year percentage change in airline seat capacity, 1H&2H2019 and weekly in 2020

Among world regions, Latin America now has the deepest cut

Europe's 84.6% year-on-year fall in total seat numbers this week is no longer the deepest cut among world regions. Latin America has taken over from Europe, with a cut of 88.7%.

Asia Pacific continues to have the lowest rate of decline, a reduction of 51.6%, while North America, Africa and Middle East have all been reduced by between 79% and 81%.

Percentage change in passenger seat capacity by region, week of 18-May-2020 vs 20-May-2019

Asia Pacific, Europe and North America are on an upward trend; other regions decline

Asia Pacific seat capacity has now been on an upward trend for four successive weeks, while North America and Europe are also following an upward curve, albeit more modestly.

However, Latin America, Middle East and Africa all reached new lows in terms of the year-on-year percentage cut in seat capacity.

Year-on-year percentage change in passenger seat capacity by region, week of 30-Mar-2020 to week of 18-May-2020

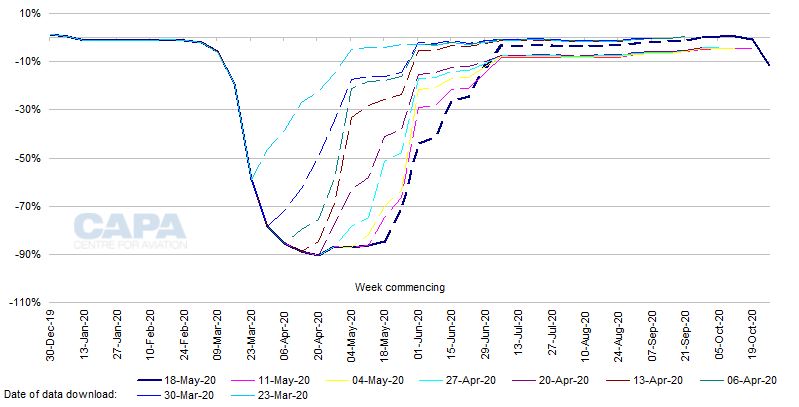

The U-shaped recovery is still widening, with Jun-2020 capacity falling…

Again, the upward arm of the U-shaped recovery depicted by schedules data continues to widen across the summer season. Capacity for Jun-2020 is now projected to be down by 34% year-on-year, compared with a 25% decline anticipated last week.

The outlook for Jun-2020 capacity implied by filed schedules data has fallen by 19% over the past two weeks.

…but Jul-2020 scheduled capacity has increased

However, projected capacity for Jul-2020 has increased by 4% compared with last week's schedules data and is now expected to be within 6% of Jul-2019 levels.

Projected capacity for Aug-2020 and Sep-2020 has increased by 5% since last week. Sep-2020 seat numbers are now expected to be within 2% of Sep-2019 levels.

Europe: year-on-year % change in airline seat capacity, with outlook at different dates*

However, the operations actually flown by Europe's airlines in the summer peak months are likely to be at much lower capacity than current schedules imply.

Scenarios published by ICAO for year-on-year seat capacity reductions in Europe in Sep-2020 range from -82% to -12%. IATA expects global RPKs to remain below 2019 levels throughout 2020, 2021 and 2022.

Schedules for Europe's big five airline groups are way ahead of likely reality this summer

Each of Europe's big five airline groups has schedules filed with OAG for the peak summer months that are wildly optimistic when compared with these scenarios from global aviation bodies. They are also far in excess of plans indicated by the groups themselves.

Ryanair, Europe's largest airline group by 2019 passenger numbers, said on 18-May-2020 that it expects to operate less than 1% of its originally planned flying programme in the Apr-2020 to Jun-2020 quarter.

It plans to increase its operations in the Jul-2020 to Sep-2020 quarter, but with no more than 50% of its original traffic target of 44.6 million passengers.

However, capacity for Ryanair Group derived from OAG schedules and CAPA seat data is projected to be above 2019 levels from Jun-2020 onwards.

Air France-KLM said on 7-May-2020 that it expected to have reduced its capacity by 95% year-on-year in 2Q2020, and by 80% in 3Q2020. Its outlook for 2021 is that its capacity will be at least 20% below 2019 levels.

OAG/CAPA seat capacity for Air France-KLM is back to/slightly above 2019 levels from Jul-2020 onwards.

Lufthansa Group has not yet indicated its capacity plans for the rest of this year. However, it has announced plans to operate around 1,800 weekly round trips, or 3,600 frequencies, by the end of Jun-2020.

This is 86% below the more than 25,000 frequencies of the final week of Jun-2019.

OAG frequency data for Lufthansa Group are only 7% below last year for the last week of Jun-2020 and back to 2019 levels from Jul-2020 onwards.

On 7-May-2020 IAG said that it was planning a "meaningful" return to service in Jul-2020, with total passenger capacity down by c.50% for the whole of 2020. It did not expect to return to 2019 demand levels before 2023.

Since then, the UK government's plans to introduce 14-day quarantine requirements on international arriving passengers prompted IAG CEO Willie Walsh to speculate that British Airways' capacity return plans may have to be pushed back.

IAG did not give details of the phasing of its capacity return through the year, but it cut capacity by around 10% in 1Q2020 and more than 90% in 2Q2020. If it is to achieve an average cut of 50% for the year, this suggests a cut of greater than 50% in 3Q2020 and a lesser cut in 4Q2020.

OAG/CAPA seat capacity for IAG is 4% above 2019 levels from the week of 6-Jul-2020 onwards.

EasyJet grounded its fleet at the end of Mar-2020. It has not announced capacity plans for the year, but has deferred 24 Airbus deliveries for FY2020, FY2021 and FY2022.

OAG/CAPA seat capacity for easyJet plc jumps from zero in the week of 25-May-2020 to 7% above 2019 levels from Jun-2020 onwards. Even without guidance on capacity plans from the airline, it is clear that the schedules outlook is vastly inflated.

There will be further cuts to filed schedules

Europe's slow and tentative rebuilding of airline capacity is just starting. However, it will not follow a straight line and may suffer some reversals on the way, depending on the ending of travel restrictions and the return of customer confidence.

Moreover, it will not follow the steep incline in schedules data.

The indicated OAG/CAPA capacity reduction of approximately 6% year-on-year for Jul-2020 compares with cuts that can be inferred from announcements by Ryanair, IAG, Lufthansa and Air France-KLM of around 50% to 80% at that stage of the year.

Airlines are filing planned schedules into the summer peak in anticipation/hope of the lifting of travel restrictions and in order to provide themselves with options for possible operations.

This makes sense, but it points to further significant reductions in the level of operations implied by European airline schedules data for summer 2020.