LCC PLAY emerges as Icelandair undergoes a resurgence

Before COVID-19, Iceland had been one of Europe's most dynamic markets, characterised until 2018 by strong growth.

The national airline Icelandair grew at double digit rates, with a North Atlantic connecting strategy via its Reykjavik hub. WOW air entered in 2012 with a similar approach at low cost and grew even more rapidly. The point-to-point market also attracted other European LCCs.

However, fierce competition weighed on both Icelandic operators, who fell into losses before WOW air's overexpansion led to its bankruptcy in Mar-2019. Icelandair started restructuring, but then the COVID crisis struck.

Iceland has now reached 71% of seat capacity for the equivalent week of 2019, similar to the Europe average of 73%, but only 50% of 2018 capacity levels (i.e. before WOW's exit). The new airline entrant PLAY aims to fill WOW's low cost role, but that will take time.

Icelandair has grown its seat share, of a smaller market, since before the crisis and also returned to profit in 3Q2021 - both rare achievements among Europe's legacy airlines.

As the coronavirus crisis recedes and the recovery builds, competition is also likely to grow in Iceland.

- Iceland's aviation market experienced strong growth before the COVID-19 pandemic, driven by Icelandair and WOW air.

- WOW air's bankruptcy in 2019 and the subsequent COVID-19 crisis led to a significant contraction in Iceland's aviation market.

- Iceland is currently operating at 71% of its 2019 capacity, slightly below the European average of 73%.

- Icelandair has grown its seat share in the Icelandic market since 2018 and returned to profit in Q3 2021.

- The new airline entrant, PLAY, aims to fill the low-cost gap left by WOW air but will face challenges in establishing itself.

- As the COVID-19 crisis recedes, competition is expected to increase in Iceland's aviation market.

Summary

- Iceland is now at 71% of 2019 capacity levels, while Europe is at 73%.

- Iceland is at only 50% of capacity for 2018 (before WOW air's exit).

- Europe is Iceland's most important market. Icelandair has grown Iceland-Europe seat share since 2018.

- Icelandair fell into losses in 2018; WOW air's 2019 exit gave little relief before the COVID crisis. Icelandair returned to profit in 3Q2021.

- The new airline entrant PLAY aims to fill the low cost gap left by WOW air.

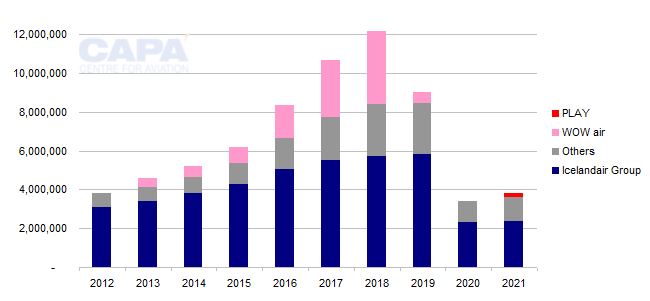

Iceland capacity grew by 13% pa CAGR 2012 to 2018, but fell by 26% in 2019 when WOW air collapsed

Total seat capacity to/from/within Iceland grew at a six-year compound average growth rate (CAGR) of 21% pa from 2012 to 2018. This was driven by strong growth from the national airline Icelandair Group, which grew at an average of 13% pa over this period but was turbocharged by WOW air.

The 2012 low cost start-up achieved a six-year CAGR of 117% pa and had a seat share of 30.9% by 2018. However, it fell victim to overexpansion and went bankrupt in Mar-2019.

Icelandair Group's seat share fell from 80.4% in 2012 to 47.1% in 2018, partially recovering to 64.9% in 2019.

COVID-19 led to further contraction in 2020, but growth is projected for 2021

In 2019 the Icelandic market contracted, with seat numbers dropping by 26% year-on-year as a result of WOW air's exit.

In 2020 the COVID-19 crisis led to a further year-on-year plummeting of 62%. Icelandair Group's share rose to 67.1% in this smaller market.

However, projections based on currently filed schedules indicate growth of 11% year-on-year in 2021 (but only to 42% of 2019 seat capacity).

Another new start Icelandic airline, PLAY, is projected to capture a seat share of 5.2%, while Icelandair Group's share is projected to slip back to 62.0% (in spite of low single digit growth in absolute terms).

Iceland: annual seat capacity 2012 to 2021*

Iceland is now at 71% of 2019 capacity levels, while Europe is at 73%

In the week of 8-Nov-2021 seat numbers in Iceland are 70.6% of the capacity of the equivalent week of 2019. This is slightly below the European average of 72.8%.

However, because of WOW air's collapse in Mar-2019 the Iceland market had already contracted significantly before the pandemic. Whereas total Europe capacity had been 97.6% of 2019 levels in the first week of Mar-2020 - just before the crisis had its full impact - Iceland capacity was then at only 78.5%.

For most of the period of the pandemic Iceland has been at lower percentages of 2018 seat capacity than has Europe as a whole.

Since late Aug-2021, Iceland capacity has been in a range of 70%-79% of 2019 levels, similar to where it was in the first two months of 2020.

Iceland is at only 50% of capacity for 2018 (before the WOW air exit)

Comparison with 2018 - the last full year before WOW air left the market - shows that Iceland is only at 50.3% of 2018 capacity in the week of 8-Nov-2021.

This compares with 73.0% of 2018 levels just before the pandemic crisis in the first week of Mar-2020.

Iceland: weekly seat capacity as a percentage of the equivalent week of 2019 and 2018, 30-Dec-2018 to 01-Nov-2021

757" height="404" />

757" height="404" />

Europe is Iceland's most important market

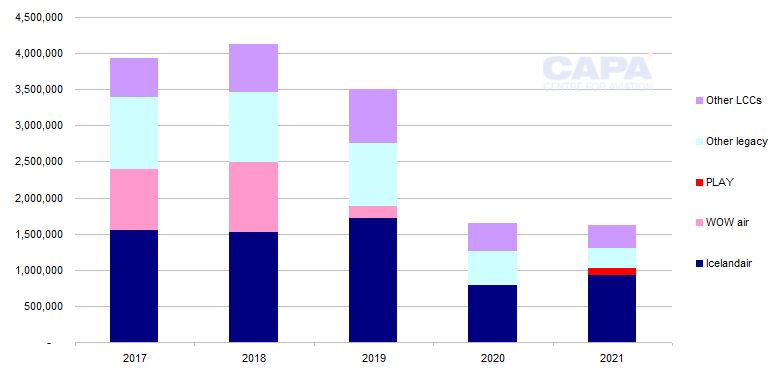

The most important market for Iceland is Europe, which accounted for 66% of seats in 2018 (almost entirely on international routes).

Following WOW air's exit, Iceland-Europe's seat share increased to 74% in 2019. In 2020 it increased to 85% as intercontinental travel became highly restricted.

However, in absolute terms, 2021 capacity on Iceland-Europe is projected to be only 46% of 2019 seat numbers (although this is higher than the 42% projected for all Iceland capacity).

Iceland to Europe: annual one-way seat capacity, 2017 to 2021*

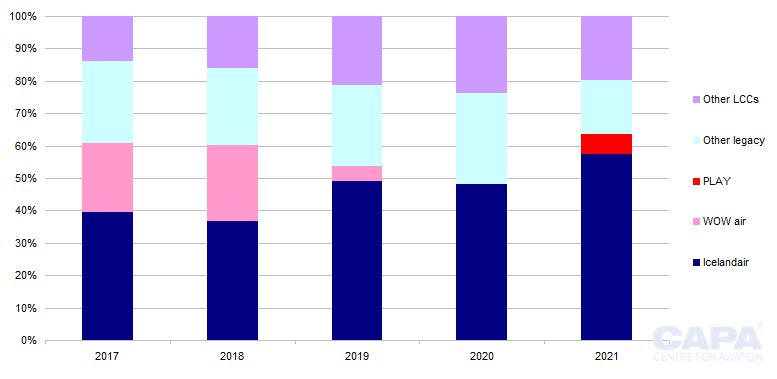

Icelandair has grown Iceland-Europe seat share since 2018

In 2018 Icelandair had c.37% of Iceland-Europe seats, while WOW air had c.23%. Other legacy airlines had c.24%, and other LCCs had c.16%.

In 2019 Icelandair's share grew to c.49% and other LCCs' share increased to c.21% as they filled some of the gap left by WOW air.

Icelandair held its Iceland-Europe seat share almost steady at 48% in 2020 and has further increased its share to c.57% in 2021, albeit a share of a much reduced market.

Other LCCs - led by Wizz Air and easyJet - grew their share to c.24% in 2020, but this has fallen back to c.20% in 2021 as PLAY has claimed c.6% of the Iceland-Europe market. Other legacy airlines' share is down from c.28% in 2020 to c.17% in 2021.

Although other LCCs have lost some seat share in 2021, their 20% share is more than the 16% they had in 2018 when WOW air was still operating.

Nevertheless, Icelandair has gained 20ppts of seat share from 2018 to 2021.

Iceland to Europe: annual seat share, 2017 to 2021*

Iceland-North America grew more rapidly when WOW air was operating

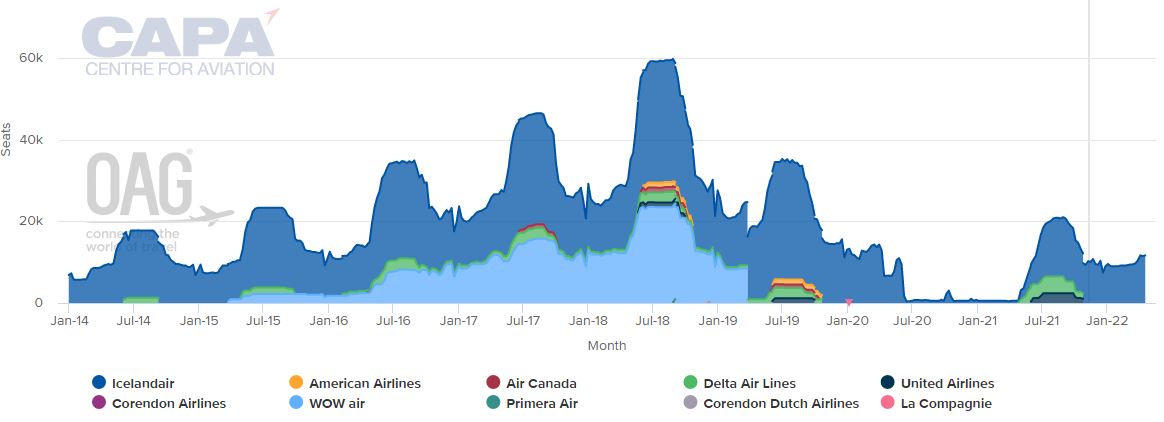

Iceland to North America capacity grew rapidly after WOW air entered in summer 2015.

This led to a period of strong competition with Icelandair as both airlines used the Reykjavik hub to pursue connecting traffic between Europe and North America in addition to point-to-point markets between Iceland and its two nearest continents.

Weekly capacity from Iceland to North America grew almost threefold between Jul-2013 and Jul-2018, compared with a 58% increase in Iceland-Europe capacity over that period.

In 2018 WOW air had c.42% of Iceland-North America seats. Icelandair had 51% - down from almost 100% in 2014 (its only competitor then was Delta, which had c7% seats, only in the peak summer months).

Icelandair's seat share bounced back to 81% in 2019 as WOW air left the market, and then 100% of a much smaller market in 2020. In 2021 the return of Delta and United has pushed Icelandair's seat share down to 75%.

Iceland to North America: weekly one-way seat capacity, Jan-2017 to Apr-2022

Icelandair and WOW air had significant overlap

Icelandair Group keenly felt the competitive impact of WOW air's rapid growth.

Based on analysis of data from OAG for the week of 30-Jul-2018, Icelandair and WOW air the two airlines overlapped on 19 routes in that summer, out of a total of 60 unique routes operated between them. Nine of the overlapping routes were to Europe and 10 were to North America.

The 19 routes represented 42% of Icelandair's 45 routes and 56% of WOW air's 34 routes last summer.

In terms of capacity overlap, the figures were higher: 49% of Icelandair's seats were on routes also operated by WOW air, and 70% of WOW air's seats were on routes also operated by Icelandair in summer 2018.

See related report: Icelandic airlines: WOW air over-inflated - and burst

Icelandair fell into losses in 2018; WOW air's 2019 exit gave little relief before the COVID crisis

The heat of competition pushed Icelandair Group into loss in 2018, the group reporting an operating margin of -3.8%, after three years of declining profitability. Its operating margin had been 11.9% in 2015, when Icelandair had been one of Europe's most profitable airlines.

It tried to buy WOW air in late 2018, but this fell through. When its rival then collapsed, the relief that Icelandair felt was short-lived, coming less than a year before the COVID-19 crisis.

The airline embarked on a restructuring programme and narrowed its operating loss margin to -2.6% in 2019.

However, the pandemic led to a collapse in traffic and revenues and a much heavier operating loss margin of -83.7%.

Icelandair returned to profit in 3Q2021

As is the case for all airlines, 2021 has continued to be a difficult year for Icelandair. However, it managed a positive operating profit in 3Q2021, with a margin of 3.2% - a better performance than many legacy airlines in Europe.

Icelandair has done well to emerge from the crisis with a higher seat share of Iceland-Europe and Iceland-North America than it had before, even if both markets have shrunk considerably.

The airline's return to profit in 3Q2021 is also creditable. However, as the crisis recedes it will face renewed competition from European LCCs and, to some extent, from the US majors.

PLAY aims to fill the low cost gap left by WOW air

WOW air demonstrated that there is a market for an Icelandic low cost airline, but its growth was too rapid, and it could not generate profits or securely fund its expansion.

The new airline entrant PLAY, with former WOW air executives as founders, says it has learnt from the defunct operator's experience and advocates a more cautious approach to growth.

It has established its presence quickly and is set to take a noticeable (6%) share of Iceland-Europe this year, after entering only in late Jun-2021.

PLAY also plans to operate Iceland-North America routes and is partly inspired by WOW air's connecting strategy. It has received initial approval to launch US routes in summer 2022, aiming at New York, Boston and Washington DC.

It currently operates three Airbus A320s and is planning to grow the fleet to between six and eight A320s/321s in 2Q2022, and more than 15 aircraft by 2025. This would actually be more than WOW air's 12 aircraft in its fifth year of operation, of which three were widebodies.

According to OAG, all five of PLAY's routes operated in the week of 8-Nov-2021 are also operated by Icelandair (Copenhagen, Berlin, Paris CDG, Tenerife Sur and London - although PLAY serves Stansted, whereas Icelandair flies to Heathrow).

As the crisis recedes, competition will grow in Iceland

Iceland is likely to continue to attract strong competition, and no doubt LCCs from outside Iceland will grow further as the post-COVID recovery gains momentum.

Wizz Air, easyJet, Transavia, Vueling, Jet2.com and Norwegian all operate to Iceland. They have lost some seat share in 2021 versus 2020, since Iceland's recovery is currently being led by its home-grown operators. However, the threat of foreign LCCs should not be ignored.

As COVID-19 becomes more and more part of normal life and aviation grows back towards pre-crisis traffic levels, the competitive challenge will resume more keenly. The next 12 to 24 months will be crucial for Iceland's two main airlines.